Delta Neutral Trading Explained

Disclaimer: All ticker prices, premiums, and return calculations shown are examples for educational purposes and reflect market conditions at the time of writing. They are not trade recommendations. Options trading involves significant risk of loss. Past performance of any strategy does not guarantee future results. Consult a licensed financial professional before trading.

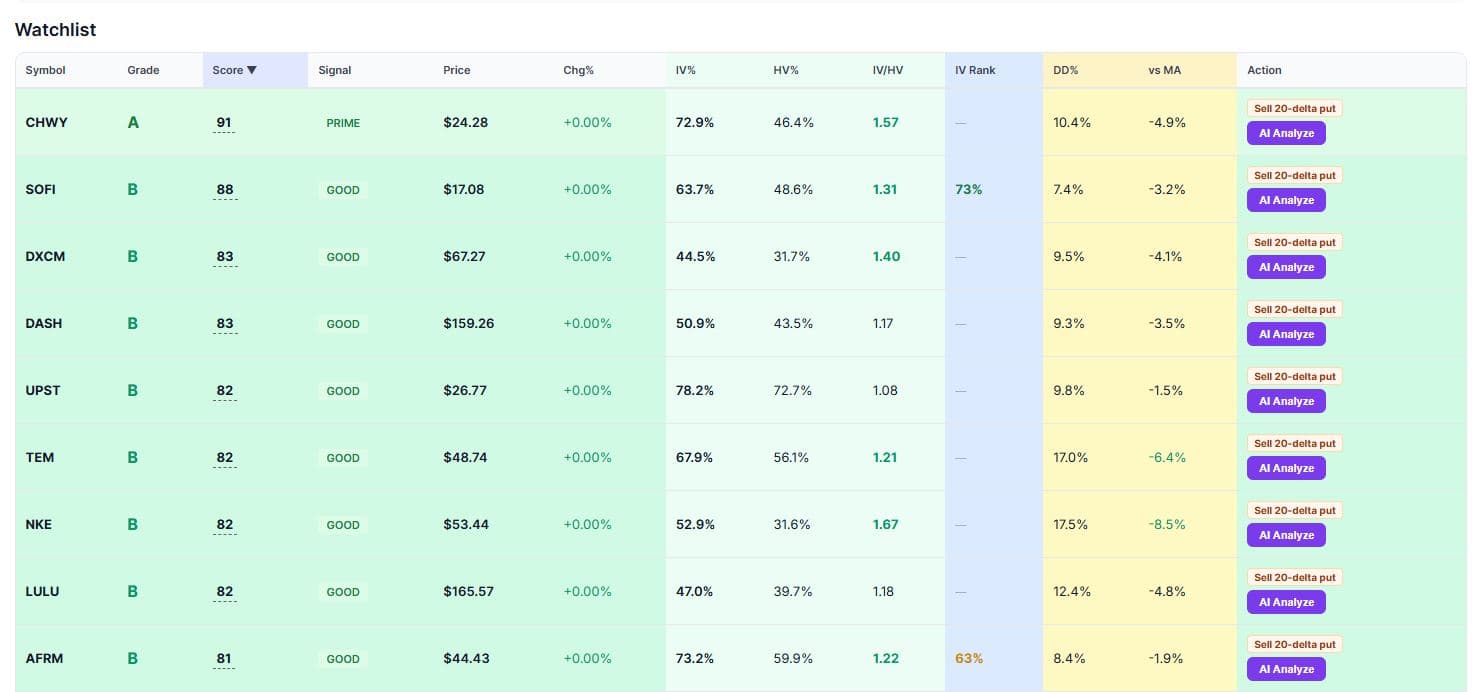

You sell the SOFI $16 put for $0.54. SOFI drops 2% the next day and your option is suddenly worth $0.90 — even though the stock only moved 34 cents. Something is amplifying the move. That something is delta hedging by market makers, and understanding how it works is the difference between getting blindsided by outsized options moves and using them to your advantage.

What Does Delta Neutral Mean?

Delta measures how much an option's price changes for every $1 move in the stock. A call with 0.40 delta gains $0.40 when the stock rises $1. A put with -0.30 delta gains $0.30 when the stock falls $1.

A delta neutral position is one where the total delta across all positions nets to zero. The position doesn't profit or lose from small stock moves. Instead, profits come from other factors — time decay (theta), changes in implied volatility (vega), or large sudden moves that trigger gamma effects.

You don't need to trade delta neutral yourself. But understanding how the biggest players in the market — market makers — maintain delta neutrality explains the hidden forces driving every option you trade.

How Market Makers Delta Hedge

Market makers are the counterparty to most options trades. When you buy a call, a market maker is typically selling it to you. They don't want directional exposure — they want to profit from the bid-ask spread and from collecting theta. So they hedge.

Here's how it works with real numbers: A market maker sells 100 call contracts on GME (currently at $22.57) with a 0.40 delta. That's 10,000 shares worth of exposure (100 contracts x 100 shares x 0.40 delta). To neutralize it, they buy 4,000 shares of GME at $22.57.

Now their position is delta neutral — if GME goes up $1, the calls lose ~$4,000 but the shares gain ~$4,000. If GME drops $1, the opposite happens. They're flat on direction and collecting the spread plus theta.

The catch: delta isn't fixed. It changes as the stock moves. That's gamma.

Gamma: Why Delta Hedging Never Stops

Gamma measures how much delta changes for every $1 move. It's the second derivative — the rate of change of the rate of change. This matters because market makers have to continuously re-hedge as delta shifts.

When GME rises from $22.57 to $24, the call delta increases from 0.40 to maybe 0.55. The market maker now needs 5,500 shares instead of 4,000, so they buy 1,500 more shares. If GME drops back to $21, delta falls to 0.30, so they sell 1,000 shares.

This creates a mechanical pattern: market makers buy shares when the stock rises and sell shares when the stock falls. They're always chasing the move, and they're doing it with size. This hedging activity amplifies moves in both directions.

Delta Hedging in Action

Watch how a market maker adjusts their share position as the stock moves. This is the mechanical force behind options pricing.

When stocks rise, market makers buy shares to hedge (pushing prices higher). When stocks fall, they sell shares (pushing prices lower). This feedback loop is why options activity drives stock price movement — and why watching institutional flow matters for premium sellers.

The Gamma Feedback Loop That Moves Markets

Here's where this gets directly relevant to your put selling. Market makers are typically net short puts — they've sold puts to portfolio hedgers and institutions buying downside protection. When stocks drop:

1. Put deltas increase (puts go further in-the-money) 2. Market makers must sell shares to reduce their now-excessive long delta 3. The selling pushes the stock down further 4. Which increases put deltas more 5. Which forces more share selling

This feedback loop is why stocks sometimes crash harder than the news warrants. It's not panic — it's mechanical gamma hedging. The March 2020 crash, the August 2024 unwind, the sudden selloffs that seem to come from nowhere — gamma hedging amplified all of them.

The flip side is equally powerful. When stocks bounce from oversold levels, market makers buy shares back (reducing their hedge as puts go out-of-the-money), which pushes prices higher, which triggers more buying. This is the snap-back rally that premium sellers love — it's the mechanical unwind of the same gamma hedge that drove the selloff.

Why IV Spikes When Stocks Drop

This gamma hedging mechanic explains something that confuses every new options trader: why does implied volatility spike when stocks crash?

It's not just fear. Market makers who are short puts and getting squeezed by the gamma feedback loop need to widen their bid-ask spreads to compensate for the increased risk of hedging. They also raise the prices of puts they're willing to sell to reflect the higher cost of continuously re-hedging in a falling market.

The result: IV spikes. And this creates the richest premium selling environment. Right when the gamma loop has exhausted itself and selling pressure starts to fade, IV is at its highest and put premiums are fattest. This is the exact moment Flow Proof's IV Rank metric lights up — when IV is elevated relative to its recent history, you're selling options at the best possible price.

Look at the scanner right now: SOFI at 47.9% IV with an IV/HV ratio of 1.36. That means implied volatility is 36% higher than what SOFI has actually been doing. Market makers are overcharging for insurance because of the gamma dynamics described above. That spread between implied and realized vol — the volatility risk premium — is the statistical edge every premium seller is harvesting.

GEX, Max Pain, and What They Tell You

Two concepts that directly flow from delta neutral mechanics:

Gamma Exposure (GEX) measures the aggregate gamma across all open options at each price level. When GEX is positive at a price, market maker hedging acts as a stabilizer — moves get dampened because hedging flows push back against the direction. When GEX is negative, moves get amplified. Negative GEX environments are where the surprise selloffs happen.

Max Pain is the price where the most options expire worthless, causing maximum loss for option holders and maximum profit for option sellers (including market makers). As expiration approaches, delta hedging by market makers can create a magnetic pull toward max pain. Stocks tend to pin near max pain more often than random chance would predict.

For put sellers, both concepts are practical: positive GEX at your strike means the stock is more likely to stay near that price. Max pain above your strike means expiration has a structural tailwind pulling the stock up and away from your danger zone.

Delta Neutral Strategies for Retail Traders

You don't need to delta hedge like a market maker. But you can use delta neutral strategies when you want to profit from volatility itself rather than direction:

Iron Condors: Sell an OTM call spread and an OTM put spread simultaneously. Your net delta is near zero. You profit if the stock stays within a range and theta decays both spreads. This is the most popular delta neutral retail strategy.

Straddles: Buy an ATM call and ATM put. You're paying for gamma — you want a big move in either direction. This is the opposite of iron condors. Useful before earnings or major events when you expect the expected move to be wrong.

Strangles: Same concept as straddles but with OTM options. Cheaper entry but requires a bigger move to profit.

Calendar Spreads: Sell a near-term option and buy a longer-term option at the same strike. Near-term theta decays faster, so the spread widens. This is a pure theta play with near-zero delta.

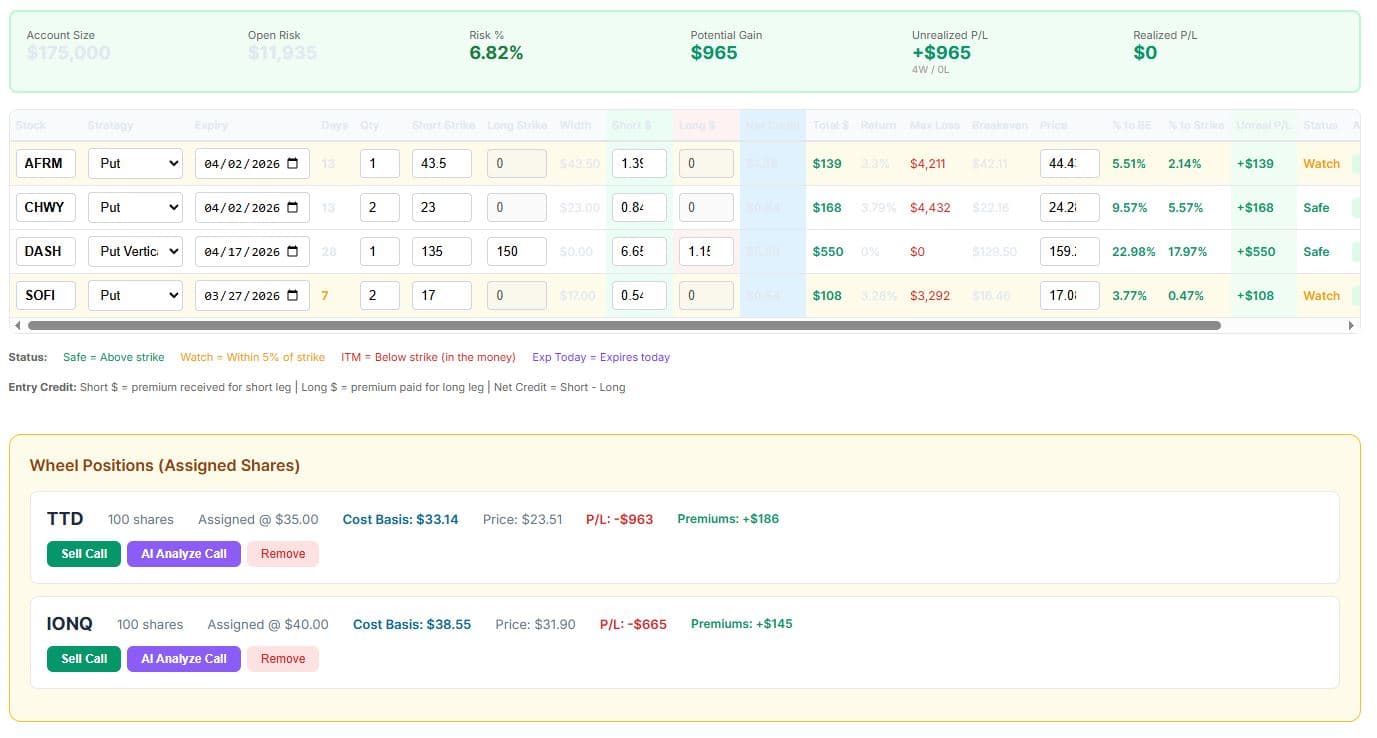

The key insight from uncleBu's framework: if you're selling options and using theta as your edge, understand that the advantage is statistical and only realized over many trades. One iron condor is not a strategy — 50 iron condors over 12 months with consistent sizing and defined risk is a strategy.

How Delta Neutral Thinking Improves Your Put Selling

Even if you never trade a straddle or iron condor, understanding delta neutral mechanics makes you a better cash-secured put seller. Here's why:

Timing entries: After a gamma-driven selloff, IV is elevated and the mechanical selling pressure is fading. This is the best environment for selling puts — you're collecting inflated premium at the exact moment the gamma feedback loop is reversing from headwind to tailwind.

Strike selection: If max pain is at $24 and you're selling the $22 put on a stock at $23, the gamma hedging dynamics are working in your favor as expiration approaches. The stock has a mechanical tendency to drift toward max pain, which is above your strike.

Flow confirmation: When you see BULLS 1sw (one institutional sweep on the call side) on GME at $22.57 in the scanner, that's not just a sentiment signal — it means someone is forcing a market maker to buy shares to hedge those calls. That hedging flow creates buying pressure. BEARS flow means the opposite — put buying forces share selling. The Flow column in the scanner is literally showing you the direction of future gamma hedging flows.

Position sizing: In negative GEX environments, consider selling fewer contracts or going further out of the money. The amplified moves can blow through strikes that normally feel safe. In positive GEX environments, you can be more aggressive because market maker hedging is working as a cushion.

Key Takeaways

Related Research & Tools

Try the Free Put Scanner

Flow Proof shows you which way institutional money is flowing — so you know whether market maker hedging is working for or against your put positions.

Open Scanner →Frequently Asked Questions

Do I need to trade delta neutral to benefit from understanding it?

No. Most retail premium sellers trade directionally (short puts = bullish). Understanding delta neutral mechanics helps you time entries, pick better strikes, and avoid selling into environments where gamma amplification is likely to blow through your position. You don't trade delta neutral — you use it as a lens.

What is gamma scalping?

Gamma scalping is a delta neutral trading technique where you buy options (long gamma) and hedge with shares. As the stock moves, you buy shares on dips and sell on rips to maintain delta neutrality. Each hedge captures a small profit from the stock's movement. It works when realized volatility exceeds implied volatility — the opposite of when premium selling is profitable.

What is the relationship between delta neutral and the volatility risk premium?

The volatility risk premium (VRP) is the tendency for implied volatility to exceed realized volatility. This premium exists partly because of the cost of delta hedging — market makers pass their hedging costs on to option buyers through wider spreads and higher prices. Premium sellers collect this embedded cost whenever they sell options.

How do market makers make money if they're always delta neutral?

Three main ways: the bid-ask spread on every option trade, theta decay on their net short options position, and gamma scalping profits from delta hedging in choppy markets. They lose money during trending markets with high realized vol because hedging costs exceed theta collected. This is why IV rises during trends — market makers need higher premiums to compensate.

What does negative GEX mean for my short puts?

Negative gamma exposure at a price level means market maker hedging will amplify moves rather than dampen them. If your short put strike is in a negative GEX zone, a small move toward it can accelerate into a larger one as hedging flows pile on. Consider using wider strikes or fewer contracts in negative GEX environments.